February 17, 2022

- Revenues in 2021 increased to €8.5bn (2020: €8.2bn)

- Low risk result of minus €570m in second year of pandemic (2020: minus €1.7bn) – still more than €500m top level adjustment for potential Covid-related charges

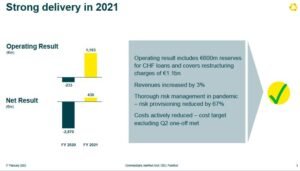

- Operating result of €1.2bn (2020: minus €233m)

- Net result positive at €430m despite restructuring charges and increased provisions for Swiss franc loans (2020: minus €2.9bn)

- Common Equity Tier 1 ratio improved to 13.6%

- Net result of more than €1bn and dividend payment planned for 2022

- Capital return policy for the coming years with pay-out ratio of 30 to 50% decided

In the first year of its transformation, Commerzbank has returned to profitability despite high one-time charges of nearly €2 billion and posted a net result of €430 million. The basis for this was the positive development of its customer business with a stabilised net interest income and a significantly higher net commission income. The Bank has also reduced its running costs as planned. Additionally, the risk result in the second year of the pandemic was significantly lower. Overall, the Bank generated an operating result of almost €1.2 billion. The Common Equity Tier 1 (CET 1) ratio improved to 13.6% providing a solid basis for the further transformation.

“In the first year of the transformation, we have delivered on our promises. We have resolutely moved ahead with our strategic initiatives. This increases our confidence that we will achieve our ambitious goals for 2024,” said Manfred Knof, Chief Executive Officer of Commerzbank. “2022 will be a decisive year in the implementation of our strategy. We intend to continue with the successful customer business of the past year and increase the net result to more than €1 billion. This means that we will aim to pay a dividend for the 2022 financial year. For the coming years, we have decided on a clear capital return policy.”

The Bank’s capital return policy provides for dividend payments in the coming years of 30 to 50% of the net result after deduction of AT 1 coupon payments. For the year 2022, a pay-out ratio of 30% is initially planned if the Bank meets its targets. Prerequisite for a dividend is a CET 1 ratio, which is at least 200 basis points above the regulatory requirement (MDA threshold) even after a dividend payment. In addition to dividend payments, the capital return policy provides for the possibility of share buybacks subject to the further successful execution of “Strategy 2024” and a regulatory approval.

Commerzbank has consistently tackled the implementation of its “Strategy 2024” in the past year, with which it intends to realign its business model to the needs of its customers, streamline the organisation, and modernise processes. Key flagship projects were successfully launched on the path to becoming the digital advisory bank for Germany. The first three advisory centres for private customers began to operate. In the Corporate Clients segment, direct banking support and services have been piloted for the first customers.

The Bank also has set ambitious sustainability goals with the net-zero target as its key element. By 2050, the net CO2 emissions of the entire loan and investment portfolio will be lowered to net zero. The Bank intends to increase its sustainable business volume to €300 billion per annum by 2025. In 2021, the volume of sustainable financial products already rose by 88% to €194 billion. With a tougher policy on fossil fuels, Commerzbank is pushing the coal phase-out and the transformation of the economy.

The Bank made important progress towards sustainably higher profitability. The framework agreement for the necessary personnel reduction was reached with the employees’ representatives, and the negotiations on the future target structure were successfully concluded. In total, the Bank will reduce headcount by approximately 10,000 full-time positions in gross terms by 2024. Especially thanks to successful voluntary and early retirement programmes, a reduction of more than 6,000 positions has already been fixed by corresponding individual contracts with employees. In total, the Bank had nearly 36,700 full-time positions at the beginning of 2022, almost 2,800 less than one year ago. To optimise its branch network, the Bank further reduced the number of locations from about 800 to around 550. This means that the Bank is progressing well towards the target size of 450 branches. Before the pandemic, the Bank had approximately 1,000 branches.

The streamlining of the international network has proceeded more quickly than originally expected. During 2021, the Bank closed 6 out of the 15 foreign locations scheduled for closure. In addition, an agreement was reached on the sale of the Hungarian subsidiary Commerzbank Zrt. Moreover, the agency network in Switzerland has already been decommissioned. To optimise its capital market business, Commerzbank entered a comprehensive cooperation in equity brokerage and equity research with ODDO BHF. Good progress has also been made to increase in capital efficiency in the Corporate Clients segment. The proportion of the business with a low RWA efficiency was reduced to a greater extent than planned – by 5 percentage points to 29% in 2021.

Commerzbank increased its revenues in the 2021 business year by a total of 3% to €8,459 million (2020: €8,186 million). This already includes the announced additional charges of €600 million for provisions in connection with the foreign currency loans of mBank. In contrast, a positive effect was seen not only from the extraordinary income from the Targeted Longer-Term Refinancing Operations (TLTRO) of the European Central Bank (ECB), but also from the contribution of almost €220 million from CommerzVentures.

A clear upwards trend was seen in securities business which led to an increase of the underlying net commission income by approximately 9% to €3,616 million (2020: €3,320 million) in 2021. Given the negative interest rate environment, the underlying net interest income amounted to €4,617 million (2020: €4,996 million). However, net interest income improved from quarter to quarter thanks to higher contributions from lending business and the expansion of pricing for large deposits.

The risk result in the past year was minus €570 million, a significantly lower level than in the previous year (2020: minus €1,748 million). The ratio of non-performing loans (NPE) improved as of the end of December to a very low 0.9% (end of December 2020: 1.0%). This confirms the high quality of the Bank’s loan portfolio. The additional provision for expected Covid effects, the so-called top-level adjustment, amounted to €523 million as of the end of the year. It remained almost unchanged compared to the end of 2020 and is still available as a provision to cover the direct and indirect effects of the pandemic.

In the past year, the total costs amounted to €6,706 million (2020: €6,672 million). This also includes the one-time write-off of €200 million for ending the outsourcing project for securities settlement in the second quarter. Excluding this one-time charge, the Bank was able to reduce its costs as planned to €6.5 billion. The operating costs were lowered by 2% to €6,039 million (2020: €6,160 million). Compulsory contributions amounted to €467 million (2020: €512 million).

The operating result increased in 2021 to €1,183 million (2020: minus €233 million); in the fourth quarter this figure was €141 million (Q4 2020: minus €328 million) despite the high additional provisions at mBank. After deduction of the restructuring expenses of €1,078 million and after taxes and minority interests, the net profit in the past year was €430 million (2020: minus €2,870 million).

The Common Equity Tier 1 (CET1) ratio improved significantly by the end of 2021 to 13.6% (end of 2020: 13.2%) due to an increase of CET 1 among others thanks to the positive net result and due to reduced risk-weighted assets (RWA). The buffer to the current regulatory requirement (MDA threshold) of 9.4% increased to around 420 basis points (end of 2020: 370 basis points).

“Thanks to the upwards trend in customer business, we were able to generate an operating result of more than €1 billion. The net result is also positive although we had to shoulder very high one-off charges. The restructuring expenses, the increase in provisions for Swiss francs loans and the extraordinary write-off due to the ending of the outsourcing of securities settlement totalled to nearly €2 billion. This shows the profit potential of our Bank,” said Bettina Orlopp, Chief Financial Officer of Commerzbank.