Fitch Ratings-Chicago/New York-23 April 2020: The US Healthcare sector overall is generally resilient but not immune to the effects of the coronavirus as the pandemic is having operational and financial implications for service providers, says Fitch Ratings. We maintain a Stable Outlook on the sector as healthcare spending is less economically sensitive than other sectors and expect post-pandemic influence on consumer behavior to be limited; thereby having fewer implications for credit profiles. However, we have taken negative rating actions on a few service providers due to the business disruption caused by coronavirus.

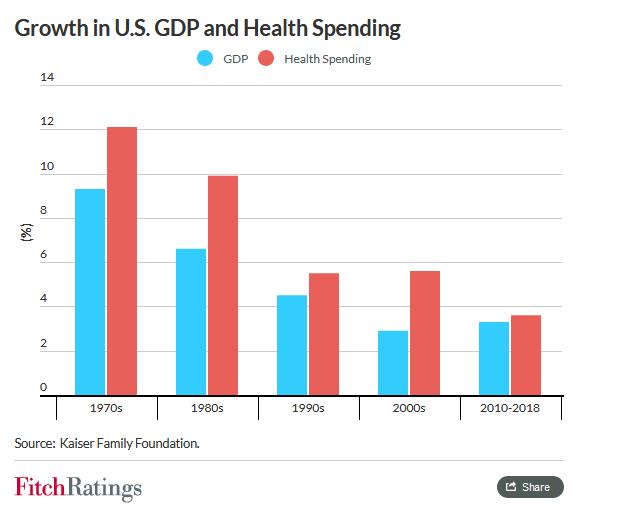

National healthcare expenditures have grown at a CAGR of 6% since 1990, consistently outpacing GDP. However, healthcare spending tends to slow during and following recessions. Spending grew at a CAGR of 2.8% in 2007–2009 during the period encompassing the last US recession. The coronavirus pandemic, however, is resulting in deep economic contraction. Fitch has revised its 2020 US GDP forecast to negative 5.6% from negative 3.3%.

To assess US corporate issuers’ vulnerability to the coronavirus pandemic, we have characterized issuers into three broad categories, taking into consideration our baseline coronavirus scenario. Reviews of companies that began 2020 with low or moderate rating headroom and moderate coronavirus exposure have been expedited, resulting in rating actions on a few healthcare providers, including Tenet Healthcare, Team Health and Quorum Health.

Tenet’s Rating Outlook was revised to Stable from Positive and Team Health’s ratings were placed on Rating Watch Negative. Quorum Health was downgraded to reflect its Chapter 11 bankruptcy filing, which was likely hastened by the effects of the pandemic on operations but not the sole precipitating factor.

Depressed volumes of patient procedures, due to delays of elective care caused by coronavirus-related business disruption, are weighing on the revenue and cash flow of service providers. This will delay expected deleveraging for Tenet and erode liquidity for Team Health if the pandemic’s duration exceeds Fitch’s baseline scenario, which contemplates an unprecedentedly weak first-half 2020. These issuers have sufficient liquidity to absorb the effects of the disruption, assuming the healthcare services sector experiences a strong recovery in elective patient volumes beginning later in 2020 and into 2021.

Demand implications resulting from the coronavirus pandemic vary across the US healthcare sector as do operational and supply-chain issues that could influence the ability to meet demand. Providers of healthcare services will see higher demand disruption, while the effect is relatively low for pharmaceuticals and variable for devices and medtech companies.

There are uncertainties in forecasting top-line growth following coronavirus-related business disruption. Uncertainties include whether there are continued outbreaks or flare ups of coronavirus hot spots. To some extent, we expect companies to be able to innovate and adapt business models to defray the business disruption. Increased use of telehealth for healthcare services is one example of potential innovation. Another uncertainty is whether demand deferred during the pandemic will be realized once operations normalize. Typically, higher unemployment results in modestly lower demand for elective healthcare services because of a loss of employer-sponsored insurance.

Despite these uncertainties, for healthcare service providers, Fitch is forecasting top-line growth of negative 5% to negative 25% for 2020, followed by a recovery in 2021 that does not bring the business back to the 2019 revenue level. For companies in lesser affected segments, such as diagnostics and life sciences, we are modeling very low growth in 2020, followed by normalized 3%-4% growth in 2021. Revenue upside exists for some segments, particularly manufacturers of coronavirus-related clinical diagnostics test and pharmaceuticals, in late 2020 and into 2020, but uncertainty about the ability of companies to realize benefits and the level of profitability limits visibility.